Last weekend it was easy to imagine that markets would be volatile this week: President Trump was set to nominate a new Fed Chairman, tax reform plans were to be unveiled, the Fed and the BOE were meeting, the post-hurricane employment reports were due, stock markets had raced to new All Time Highs…what could possibly go wrong?

Not much, apparently, as implied volatility fell back this week to near All Time Lows across asset classes…currency markets muddled mostly sideways with the US Dollar Index inching to its strongest weekly close since July…bond yields fell as the market reversed from pricing in a possibly tighter Fed…and stocks ambled to new All Time Highs!

Fed Chair: The President nominated Powell to replace Yellen when her term expires in February and the Senate is expected to approve his nomination. He provides continuity with recent Fed policies (better the devil you know…) but also showcases that Trump remains intent on “shaking things up.”

Tax Reform: There was very little reaction to the tax reform details across major stock indices, currencies and interest rates. There was, of course, a tsunami of politically motivated commentary about how bad or how good the proposals were, and whether or not the proposals will ever become law.

The Fed meeting: wasn’t expected to provide any fireworks, and didn’t. They see “solid” US economic growth and markets are now pricing a 90% chance that the Fed will raise short term interest rates by ¼ in December…and with financial conditions the “easiest” in over 2 decades the Fed may be tightening more in 2018 than the market is currently pricing…which would be USD bullish.

The employment report: was expected to show a big, possibly huge, post-hurricane employment rebound…but the net market effect of the report was subdued. Jobless claims fell to a 44 year low.

Consumer confidence: reports this week showed that American consumer confidence is at a 15 year high due to gains in the stock market, housing prices and wages(?) Consumers are now 70% of US GDP so their high confidence level may have a positive feedback effect on the stock market and housing prices…although I have to wonder if this isn’t a classic “end of cycle” picture especially with consumers running down their savings and going deeper into debt so that they can keep buying things! Another cautionary sign is that the growth rate for national wages is about half the growth rate for national housing prices.

The Canadian Dollar: One of the primary drivers of CAD-USD since May has been the 2 year interest rate spread. At the May CAD lows the spread was 65 points in favor of the USD, at the Sept 8 Key Turn Date the spread was 25 points in favor of CAD. Since early September the spread has gradually gone in favor of the USD and for the past week or so has hovered around 20 points premium USD. The 180 degree pivot by the Bank of Canada in early June, and the subsequent “backing away” by the BOC in September obviously influenced the interest rate spread and thus the FX rate. BOC Governor Poloz spoke before Parliament this week and maintained a “worried” tone. The correlation between CAD and WTI, which has been important for much of the past couple of years has been practically non-existent the past few months.

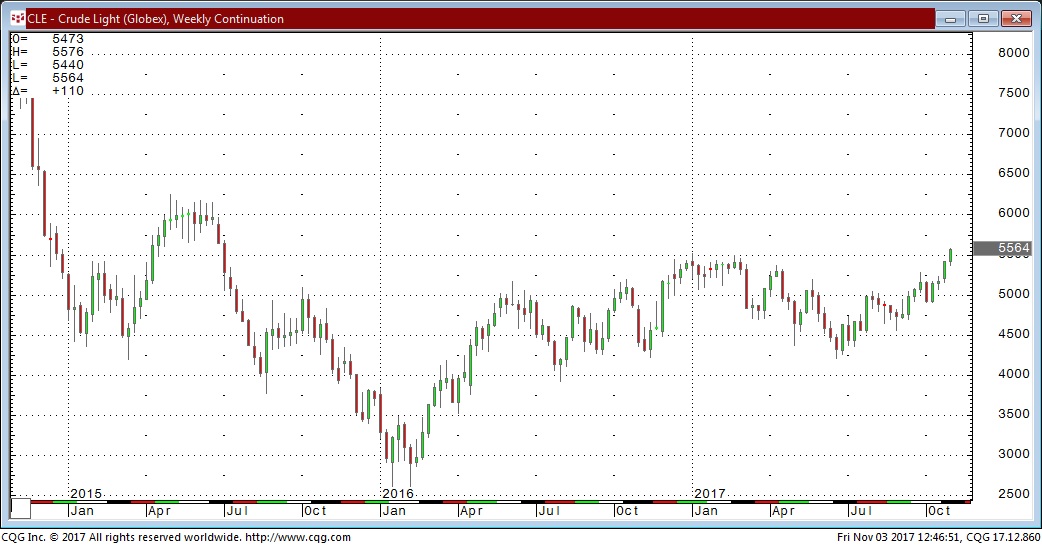

WTI: following the OPEC production cutback agreements in November 2016 and the OPEC/Non-OPEC agreements in December 2016, front month WTI topped out around $55 in January and February 2017 (I wrote that the crude oil bullish news had reached “As Good As it Gets” back then) and WTI began a stair-step decline to $42 in June. Since that June low market sentiment swung to believing that the cutback agreements have indeed reduced global supply below global demand, thus shrinking the inventory overhang, and prices have risen…with WTI closing above $55 this week for the first time in over 2 years. Rumors that the agreements will be extended when OPEC meets on November 30 have helped fuel the rally. It’s interesting that crude oil has rallied over 15% since early September even as the USD has risen against nearly all currencies. Crude oil, in other words, is rallying in terms of all currencies…a hallmark of a strong bull market.

My short term trading: My current core trading idea is that the USD made an important turn higher on September 8 after falling about 12% from a 14 year high in January. All of my trading since early September has been based on this core idea. CAD: I got short the week following September 8 and essentially stayed short until last week when I went flat. CAD had dropped over 5 cents and I felt it was due for a bounce. I re-established an initial short position when CAD rallied on Friday’s stronger-than-expected Canadian employment report. Euro: I had established short Euro positions in mid-October on the expectation that it would fall through the neckline of the head-and-shoulders pattern that had begun in late July. I covered some of that trade last week and the balance this past Monday. I bought the US Dollar index this morning following the employment report. WTI: I have traded WTI almost exclusively from the short side for the past 3 years but have been on the sidelines for the past couple of months.

PI Financial Corp. is a Member of the Canadian Investor Protection Fund. The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or the authorize someone else to trade for you, you should be aware of the following. If you purchase a commodity option you may sustain a total loss of the premium and of all transaction costs. If you purchase or sell a commodity futures contract or sell a commodity option or engage in off-exchange foreign currency trading you may sustain a total loss of the initial margin funds or security deposit and any additional fund that you deposit with your broker to establish or maintain your position. You may be called upon by your broker to deposit a substantial amount of additional margin funds, on short notice, in order to maintain your position. If you do not provide the requested funds within the prescribe time, your position may be liquidated at a loss, and you will be liable for any resulting deficit in your account. Under certain market conditions, you may find it difficult to impossible to liquidate a position. This is intended for distribution in those jurisdictions where PI Financial Corp. is registered as an advisor or a dealer in securities and/or futures and options. Any distribution or dissemination of this in any other jurisdiction is strictly prohibited. Past performance is not necessarily indicative of future results.