Trade freedom has been dominating the headlines and adding to the growing economic risks and market volatility. Trump’s tariffs on steel and aluminium imports have prompted fears of a trade war, albeit with a low probability and with some comfort offered with the exemption clauses. This does, however, remind us that negotiating with the US is difficult and that NAFTA negotiations have yet to be resolved. A more important and difficult issue is that of intellectual property rights in relation to China. For now, markets seem to be looking through the bravado because it is mutually beneficial for all sides to avoid a trade war which would negatively impact global economic growth prospects. This week we quantify trade freedoms to validate that seemingly prosaic position.

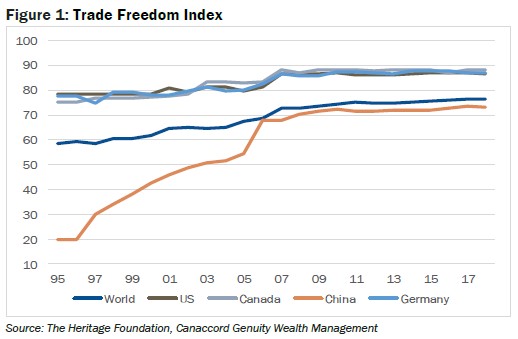

Using data from The Heritage Foundation, we see there have been notable reductions in trade barriers across the world over the past twenty or so years. Figure 1 highlights the Trade Freedom Index – for the world and four major economies. The Index is a composite measure of the absence of tariff and non-tariff barriers that affect imports and exports of goods and services. Trade freedom for the world has improved from under 60 per cent in 1995 to just under 80 per cent in 2018. The US along with Canada and Germany are close to 90% on the trade freedom score. In the case of China, there has been significant improvement from 20 per cent in 1995 to over 70 per cent in the latest measure. The rhetoric really does seem to be misplaced.

If Trump wants to bash China, maybe he should be focusing on investment freedoms (constraints on the flow of investment capital, and financial freedom which is a measure of banking efficiency and independence from government control). Measures that track investment freedoms have deteriorated over the past twenty years. We suspect that common sense will eventually prevail and that the market is correct to heavily discount the prospect of a trade war and focus instead on the improving fundamentals.

The US economy created 313,000 new jobs in February which was the biggest gain since mid-2016 according to the non-farm payrolls, a key leading indicator of economic activity. Jobs created in January and December were revised up to 239,000 and 175,000 respectively. The unemployment rate was unchanged at 4.1% last month. Average hourly earnings, which had spooked market fear of heightened inflationary pressures, rose by just 2.6 per cent year-on-year in February down from 2.8 per cent in January (which in turn was revised down from 2.9%). The inflation scare seems to have passed, but growth remains buoyant with the University of Michigan Consumer Sentiment Indicator coming in strong and with the economy projected to grow by some 2.8% annualised in Q1 2018 from 2.6% in Q4 2017 according to the Atlanta Federal Reserve GDPNow model.

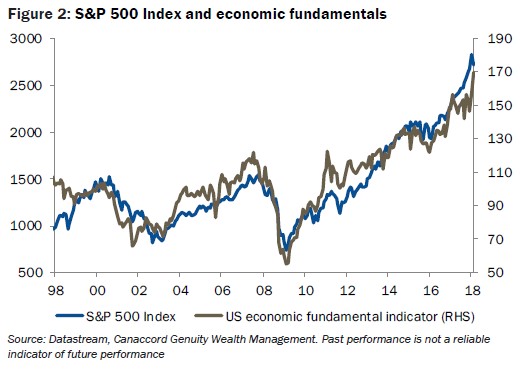

The economic fundamentals are important and we validate that in Figure 2 which highlights the close relationship between the S&P 5000 Index performance versus an economic composite indicator since 1998. The economic composite indicator is a blend of the Michigan Consumer Sentiment Index, the initial jobless claims and the CRB Spot Index. As George Michael might have said, “I think there’s something you should know…”, we should be focussing on the fundamentals and discounting the rhetoric for now.

Brent Woyat, CIM, CMT

Investment Advisor, Portfolio Manager

Canaccord Genuity Wealth Management

T: 604.699.0869 | F: 604.643.1802

All information is given as of the date appearing in this document and Canaccord Genuity Wealth Management (CGWM) does not assume any obligation to update it or to advise on further developments related. All this information has been compiled from sources believed to be reliable, but the accuracy and completeness of the information is not guaranteed, nor in providing it do CGWM assume any liability.

All views expressed in this document are provided for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities. The statements expressed herein are not intended to provide tax, legal or financial advice, and under no circumstances should be construed as a solicitation to act as a securities broker or dealer in any jurisdiction. All views are intended for general circulation to clients and do not have any regard to the specific investment objectives, financial situation or general needs of any particular person.

Forward-looking statements and past performance are not guarantees of future results. To the fullest extent permitted by law, neither CGWM nor its affiliates or any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of the information contained in this document. Canaccord Genuity Wealth Management in Canada is a division of Canaccord Genuity Corp. Member – Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada