Wealth Building Strategies

Several years ago, New York Times Wealth Matters columnist Paul Sullivan opened up his finances to a group of high-powered, high-net worth investors known as Tiger 21.

Several years ago, New York Times Wealth Matters columnist Paul Sullivan opened up his finances to a group of high-powered, high-net worth investors known as Tiger 21.

Members gather regularly to discuss investing strategies and at one meeting, Sullivan asked them to critique his own — relatively meager by their standards — financial life.

“Given what I do, I thought [my wife and I] had a handle on it, but what I learned from that meeting is that we hadn’t thought enough about the risks in life,” Sullivan says.

Those risks include declining incomes and the unexpected death or disability of a household wage earner. As a result of that meeting, Sullivan and his wife took out life and disability insurance policies and sold off a condo in Florida that had been a vacation home for the family.

“They were so direct and harsh about that being a possible drain, if we weren’t able to sell it if something bad happened. That was a wake-up call,” Sullivan says.

The lessons he absorbed from that wealthy, exclusive group of over 300 members across the U.S. and Canada led Sullivan to write his new book, “The Thin Green Line: The Money Secrets of the Super Wealthy.” The title refers to the security that can come from knowing you’re prepared for a negative event, like a layoff, no matter how much money you have or earn. “The people in the book who I call wealthy, whether they’re a teacher or a hedge fund manager, are wealthy because they have security. They have behaviors around money that let them be in control of their lives when something bad happens,” he says.

Those behaviors, Sullivan says, can be learned or even adopted later in life. As someone who grew up without much money, he says it took him a long time to have a healthy relationship with it. He would avoid credit card debt and overspending so assiduously that he often wore threadbare clothing and skipped even affordable purchases he would have enjoyed. “You should be able to spend money on things you enjoy. If you love $4 Starbucks lattes, then buy it,” he says.

If you’re looking to adopt some secrets of the wealthy, Sullivan suggests the following strategies:

…related:

Here’s an overview of six of the ways nanotechnology uses are making a big difference in our daily lives.

Here’s an overview of six of the ways nanotechnology uses are making a big difference in our daily lives.

While there’s been plenty of focus on apps and cloud computing in the technology space, advances are also being made in hardware-focused sectors such as nanotechnology. Uses include everything from more efficient drug delivery systems to tiny transistors that allow for smaller and more powerful computer chips.

To be sure, the markets for nanotechnology products and nanotechnology uses are set to grow in the coming years. A report released this past December from Research and Markets states that nanotechnology “is a rapidly growing technology” and the global industry has been forecast to grow annually by 17 percent up to 2024.

Similarly, BCC Research has said that the global nanotechnology market was valued at $39.2 billion in 2016 and should grow at a CAGR of 18.2 percent, in order that the market will reach a believed $90.5 billion by 2021.

Still, for investors just starting to look at nanotechnology stocks, it can be difficult to know where to to begin, as nanotechnology uses are so varied. As a starting point, here’s an overview of six of the top areas in which nanotechnology uses are making a big difference today.

….Click below for description and stock recommendations:

Materials & Coatings

Medicine

Food

Electronics

Energy applications

Water and air treatment

…continue for

Go through the late 2015/early 2016 articles published on this and similar sites and you’ll find a consensus that 2016 was going to be a really bad year. Corporate profits were falling, business inventories had spiked, and deflation was deepening in Japan and Europe. See More Ominous Charts For 2016 for a longer list of indicators that seemed, a year ago, to portend imminent recession if not full-blown financial crisis.

As David Stockman put it in a late-2015 prediction piece,

The Keynesian Recovery Meme Is About To Get Mugged, Part 1

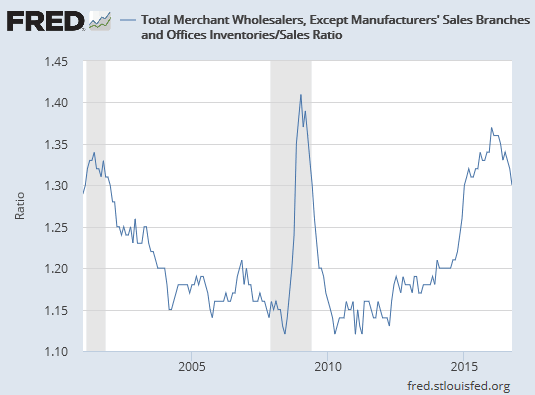

Just consider the most recent data on wholesale sales and inventory. This sector of the domestic economy embodies the leading edge of business activity, meaning that trends in wholesale level sales and inventory stocking are advance indicators of the general macroeconomic outlook.

Needless to say, the soaring inventory-sales ratio is not a sign that “escape velocity” is just around the corner. Contrariwise, whenever the ratio has busted through 1.30X in the past, what came next was a recession.

Recessions happen on the main street economy, of course, when sales weaken and inventories build to the point where liquidation of excess stocks becomes unavoidable. Accordingly, of far greater significance than the 19 labor market graphs supposedly on Yellen’s dashboard is the unassailable fact that wholesale sales have now rolled over.

The natural market driven bounce back from the deep liquidation during the Great Recession is now over and done. Wholesale sales are down 4.5% from their June 2014 peak and have returned to September 2013 levels.

Moreover, it is also well worth noting that at the most recent October 2015 level, wholesale sales are now up at only a 1.6% annual rate from the pre-crisis peak. Surely that does not measure an economy that is healed and heading toward the promised land of full-employment.

So the false conclusion about the US economy’s strength derived from the Fed’s faulty labor market telemetry cannot be emphasized enough.

There has been no Fed driven main street recovery. Instead, the tepid business expansion after the 2009 bottom embodied nothing more than the natural regenerative impulses of our badly impaired but still functioning capitalist system. As the inventories of goods and labor that were thrown overboard during the post-crisis plunge were rebuilt, incomes recovered and the cycle of expansion paddled forward on its own motion.

But that’s now done, and the US economy stands fully exposed to the albatross of peak debt and the gale forces of global deflation.

Yet here we are a year later, with US stocks at record levels, growth apparently accelerating and deflation morphing into modest inflation. What happened? Two things.

First, 2016 was a US presidential election year, and the desire to see incumbents hold power trumped whatever qualms Washington might have had about adding to its debt. So the Feds borrowed another trillion+ dollars, presumably spending it on things designed to make voters want to stay the course.

Second, the threat of deflation terrified governments from Japan to Germany, leading them to push interest rates into negative territory for a wide range of sovereign (and some corporate) bonds. Corporations, as a result, felt compelled to borrow as much as possible even if they had no material use for the money.

All this government/corporate cash sloshing around the global financial system has pushed up equity prices and led to a bit more hiring – though apparently still mostly of bartenders and waiters – that has in turn generated some good headline numbers. See Debt Surge Producing Fake Recovery.

The success of this latest bit of can-kicking leaves critics of the current system with a bad case of prediction fatigue. We’ve been tossing around terms like “unsustainable” and “imminent crisis” for so long that they’ve begun to lose both meaning and credibility.

The only consolation is that this is familiar territory. Bubbles tend to go on until most of their critics have been silenced. Tech stocks, for instance, were clearly a bubble in 1998 but didn’t pop until 2000. US housing became an obvious bubble in 2005 but didn’t pop until 2007. In each case the people who initially pointed out the danger were exhausted and/or ignored by the time they were finally proven right.

Since the current bubble – encompassing fiat currencies, government bonds and related derivatives – is by far the biggest and broadest ever, it shouldn’t be a surprise that it’s lasted well beyond what rational analysis says is possible. But it too will pop. In fact, 2017 is looking pretty bad…

….related: The Greatest Money Manager Alive Attributes The Majority Of His Success To Just This One Thing

I don’t think so. Here again, most analysts got the Shanghai Gold Exchange (SGE) completely wrong.

The SGE was established in October 2002 by China’s central bank, the People’s Bank of China (“PBOC”) upon approval by State Council and supervised by PBOC.

Officially and fully open for business in September 2014, I personally was the first foreigner to visit the SGE in October 2004 and spoke with the president. Construction was underway, communications, quote pits for the different products and more. It was an interesting visit, under armed guard.

But for the record, let me explain the myth that the SGE is going to boost gold demand and send it to the moon.

The chief reason for the SGE is to officially allow two

types of cross-border trade in gold in China:

To promote general trade and processing trade.

In a nutshell, that means the gold is not brought in to the SGE for investment …

But instead, for manufacturing or assembling purposes after which the finished goods are required to be exported.

On BullionStar.com, columnist Koos Jansen reveals the byzantine details of the Chinese gold trade:

Usually processing trade is conducted through Customs Specially Supervised Areas (CSSAs) – also called Free Trade Zones, Customs Specially Regulated Areas, Special Customs Supervision Areas or Customs Special Supervision Regions, these are all the same.

When processing trade is performed outside CSSAs (the rest of the mainland, non-CSSA) the materials will be strictly monitored by Chinese customs. Through processing trade gold cannot enter the Chinese domestic gold market where the SGE operates. Processing trade and CSSAs are strictly separated from the Chinese domestic gold market.

Processing trade is meant for China’s manufacturing industry to efficiently connect with the rest of the world. The Chinese and foreign companies engaging in processing trade are exempt from, in example, import duties and Value-Added Tax (VAT).

General Gold in China Trade

When gold is imported into the Chinese domestic market, this is referred to as general trade. The agency that controls all forms of gold in general trade is China’s central bank, the People’s Bank of China (PBOC).

Only financial institutions and gold enterprises that carry the Import and Export License of the People’s Bank of China for Gold and Gold Products (the License hereafter) can get gold to pass customs into the Chinese domestic gold market.

The rules for cross-border gold trade in general trade have been lastly drafted by the PBOC in March 2015 and are called Measures for the Import and Export of Gold and Gold Products (the Measures hereafter). In the Measures it’s stated:

For the import and export customs clearance of gold and gold products as included in the Catalogue for the Regulation of the Import and Export of Gold and Gold Products, the Import and Export License of the People’s Bank of China for Gold and Gold Products issued by the People’s Bank of China or a People’s Bank of China branch shall be submitted to the Customs.

The Catalogue for the Regulation of the Import and Export of Gold and Gold Products describes all forms of gold (coins, ore, bullion, unwrought, scraps, jewelry) that can cross the Chinese border. For all gold to be imported into the Chinese domestic gold market the material is required to be accompanied by the License.

Currently there are 15 commercial banks that are approved by the PBOC to apply for the License to import standard gold, which in China is bullion in bars or ingots of 50g, 100g, 1Kg, 3Kg or 12.5Kg, having a fineness of 9999, 9995, 999 or 995. The 15 commercial banks are:

Agricultural Bank of China

ANZ

Bank of China

Bank of Communications

Shenzhen Development Bank/Ping An Bank

Bank of Shanghai

China Construction Bank

China Merchants Bank

China Minsheng Bank

Everbright

HSBC

Industrial and Commercial Bank of China

Industrial Bank

Standard Chartered

Shanghai Pudong Development Bank

All standard gold imported through general trade into the Chinese domestic gold market is required to be sold first through the SGE (the core of the Chinese domestic gold market). In the Measures, it’s stated:

… An applicant for the import and export of gold … shall have corporate status, … it is a financial institution member or a market maker on a gold exchange [SGE] approved by the State Council.

… The main market players with the qualifications for the import and export of gold shall assume the liability of balancing the supply and demand of material objects on the domestic gold market. Gold to be imported … shall be registered at a spot gold exchange [SGE] approved by the State Council where the first trade shall be completed.

Next to standard gold there are non-standard gold (for example bullion bars weighing 200g 9999 fine and doré bars), gold products (jewelry, coins and ornaments) and ore.

Non-standard gold, gold products and ore are not required (and not allowed) to be sold through the SGE when imported into the Chinese domestic gold market. Only a limited number of gold enterprises can apply for the License to import non-standard gold, gold products and ore under general trade. Although, the Measures released in March 2015 by the PBOC loosened the requirements for such enterprises.

An example of a gold enterprise that can import non-standard gold into the Chinese domestic gold market: On May 26, 2015, Zijin Mining Group bought a 50% stake in Barrick Gold Corp’s Porgera mine in Papua New Guinea for $298 million.

On October 9, 2015, China Gold Network wrote that Zijin Mining was one of the first mining companies to be granted the qualification by the PBOC to import gold under general trade, allowing Zijin to import doré from Papua New Guinea into the Chinese domestic gold market.

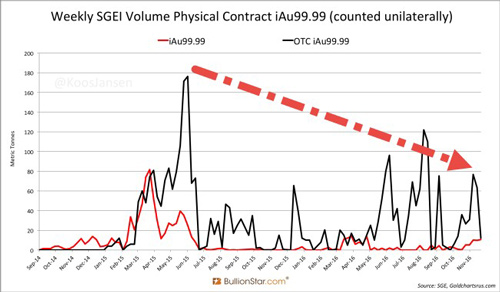

Either way, you can clearly see this is all about regulation, not boosting demand. And indeed, demand through the SGE has declined, pretty much year-over-year, per this table, courtesy of BullionStar.com

You can see the surge in trading in mid-2015, but from there on out, it’s pretty much a downtrend.

The SGE will NOT boost gold demand, at least not enough to turn a bear into a bull. And neither will the new Sharia law on gold you’re hearing about.

The only three things that will turn gold around to the upside are …

1. A crash in the dollar. Highly unlikely, though a short-term pullback is in order.

2. A collapse in global stock markets. Unlikely.

3. A new black market in gold, which is forming.

Best wishes,

Larry

P.S. Make sure to click here to download my new free report Stock Market Tsunami!

Last April I wrote a post about the specific trading style that has made guys like Stan Druckenmiller, Jim Rogers and George Soros so successful. That post focused on a single quote from Druck which I found particularly compelling because it goes against what most investment pundits would tell you is the right way to invest.

Last April I wrote a post about the specific trading style that has made guys like Stan Druckenmiller, Jim Rogers and George Soros so successful. That post focused on a single quote from Druck which I found particularly compelling because it goes against what most investment pundits would tell you is the right way to invest.

But Druck made an even more poignant and timely point in that speech a year ago. He singled out specifically what he believes to be the most important factor behind the returns in risk assets, namely the stock market:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair